Creative and enterprising people are rarely satisfied with self-employment. Realize your potential, try your hand, increase your income level allows your business. Often, entrepreneurs are primarily afraid of opening an LLC: a lot of responsibility, considerable initial capital, there are no guarantees that the business will immediately begin to gain momentum. A more suitable option for many is IP on UTII. Cargo transportation is one of the types of activity that fits this regime. Those interested are advised to read the article. We will analyze the complex in simple words.

What kind of beast "UTII"

As a support to small businesses and young entrepreneurs, the state has developed several simple taxation regimes that allow you to try your own business and save on associated costs. Now it is:

• USN (simplified mode);

• USCH;

• Patent;

• UTII.

The single imputed income tax is a taxation system in which the entrepreneur pays a fixed amount to the state, which does not depend directly on real income. Not every type of activity will fit this benefit.

There is a limited list regulated at the federal level (Article 346.26 of the Tax Code). In addition, legislative acts at the oblast level may reduce it or prohibit the use of an imputation regime in the territory entrusted to them.

Since 2021, it is planned to abolish UTII. But while it is allowed, it is one of the most popular reporting schemes to the state. bodies.

What is the optimization?

Owners of, for example, a business such as trucking at UTII avoid paying taxes:

• VAT;

• profit or personal income tax;

• on property.

In addition to these privileges, entrepreneurs without employees are saved from the fate of submitting reports to the pension fund and the Social Insurance Fund. The Federal Tax Service remains the sole control body, meetings with which are possible no more than 4 times a year. If officially registered employees are still available, then they will still have to report on insurance and funded contributions. But this is inevitable with any taxation.

The selected mode is uncomplicated. In certain conditions, a businessman can do without an accountant. Further on an example, we consider issues related to reporting and tax calculation. You will definitely know everything and not get confused in terms.

Are cargo transportation suitable for UTII?

Cargo transportation is one of the most popular types of business. According to the methods of transportation emit:

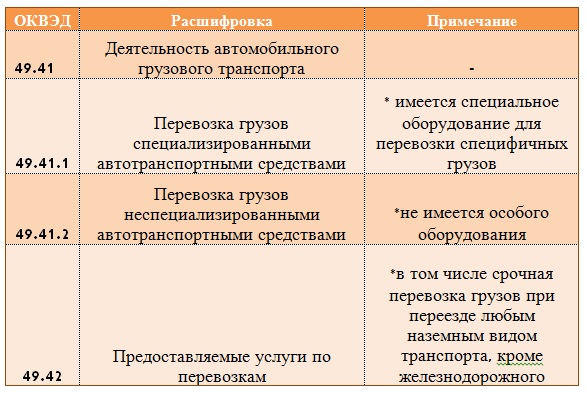

1. Automotive - the most economical option. OKVED code 49.41 (including specialized and non-specialized transport).

2. Railway are used for bulky goods or in case of large volumes. OKVED code 49.20 (includes dangerous goods and other).

3. By air, most often deliver urgent parcels. OKVED code 51.21 (including the presence / absence of aircraft schedules).

4. Water - an economical alternative to train and plane, but the time consumption increases significantly. OKVED code 50.20 (includes a large list of types of products), 50.40 (delivery by inland waters)

5. Space transportation (OKVED code 51.22.2)

Under the UTII regime, freight transportation is suitable only by road, and specifically by buses, cars and trucks (Article 346.27 of the NKRF). Therefore, OKVED can be selected from the list.

If you are engaged in other types of transportation services, then you should consider other specials. modes.

What restrictions are there when switching to UTII (Article 346.26 of the NKRF)

You cannot switch to UTII if you have:

• more than 20 vehicles;

• more than 100 people in the state;

• there are rental services for gas stations;

• activities within a partnership or trust agreement.

In addition, depending on the type of cargo and transportation routes, the businessman must be aware of the need to have licenses and permits. Since this topic is very extensive, let us leave it for a separate consideration. Keep in mind that in the absence of the necessary tolerances, the tax authority has the right to impose a fine on the entrepreneur or deprive him of the right to use the benefits.

You can go to UTII either within 5 days after registration, or from the beginning of the calendar year by submitting a request on the form. If you have not informed the Federal Tax Service about your intentions to use this special. mode, you reckon on the general. And despite the fact that your activity is suitable for "imputation", you are required to pay VAT, income tax and others.

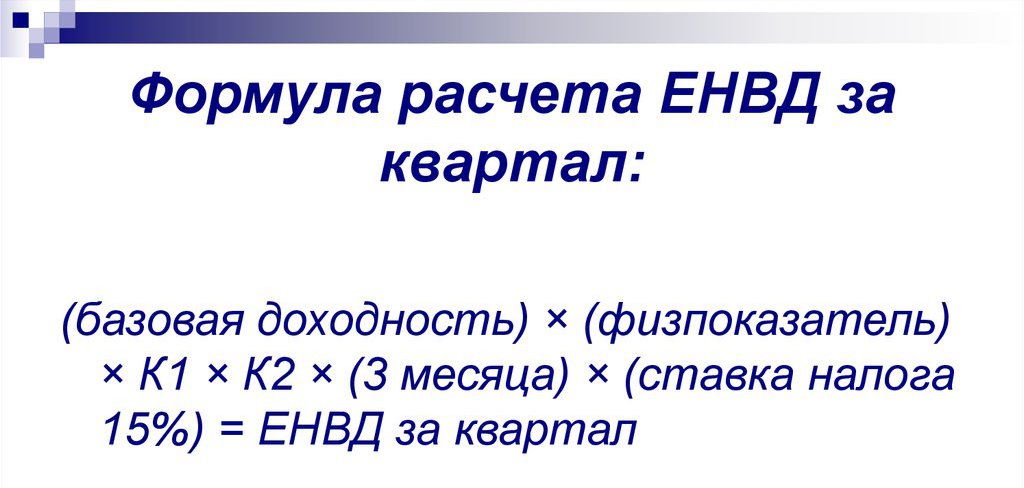

Definition of a physical indicator, basic profitability, deflator coefficients

If you are still with us, it means that your idea falls under the UTII tax regime, and freight transportation is what you decided to do. Before you make out how it is considered, you need to determine the components:

• physical indicator;

• basic profitability;

• correction factors.

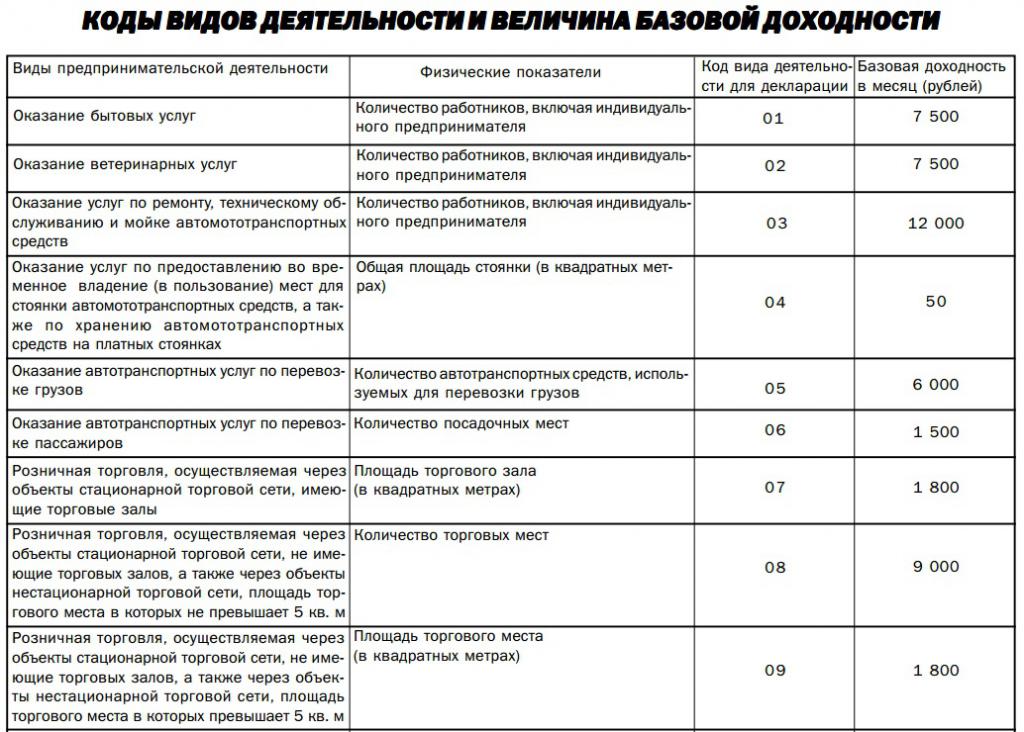

When choosing an appropriate OKVED, an individual entrepreneur should know that in the UTII declaration, freight transportation is indicated by the activity code number 05. In other words, OKVED 49.41 corresponds to code 05. Other data is tightened depending on the code.

A physical indicator implies the basis on which the calculation is based. For freight on UTII FE must take the number of vehicles used to provide services. Recall that they should not be 21 pieces or more. For other services, this may be the number of employees, and the area of the hall, and the area of the stand.

A specific physical indicator corresponds to income, which by definition should be received by the owner from each piece, meter, etc. This amount is theoretically calculated by special bodies and fixed by law (Article 346.29 of the NKRF). It can be reviewed and changed annually. Therefore, when calculating, you need to use the latest data.

Another corrective factor is special factors. There are two of them.

The K1 coefficient is approved by the Ministry of Economic Development annually. It depends on inflation and average consumer prices. K1 is fixed for the next year by the order of the Ministry of Economic Development around October-November of the current year. For 2019, for example, it is planned to establish 1.915 (which is slightly more than 2018 - 1.868).

K2 - established by local authorities. It, in turn, depends on:

• type of activity;

• average earnings of employees;

• places of business.

The decision on this coefficient is not adopted annually by the City Duma. That is, the calculation rules and numbers corresponding to it can be established for several years. It varies following the changing business environment from quarter to quarter.

How to calculate for UTII FE for freight?

Take for example this situation. Activities are carried out in the city of Togliatti (Samara region). Cargo delivery is carried out on a single car. The state has only one person - an entrepreneur. Carrying out cargo transportation SP on UTII.

Taxes are calculated as follows.

We have already decided that for the type of cargo transportation activity, the physical indicator is the number of cars. In this case = 1. We are looking in article 346.29 of the NKRF for the value of the basic return for transport services. It is equal to 6000 rubles.

The K1 coefficient for 2018 was set by the Ministry of Economic Development equal to 1.868.

K2 is calculated by the formula (by decision of the City Council of the city of Togliatti dated 10.16.13):

K2 = V * Z * F, where

V - depends on the type of activity, and in this example = 1;

Z - is determined by the salary of employees. Having no data on the cost of living for the region, etc., we take the maximum possible value = 1;

F - place of business. The farther from the city center, the lower the value. Since the activity is carried out in the city of Togliatti, the value is 1.

Total K2 = 1 x 1 x 1 = 1

In the final value, we have: (6000 x 1 x 1.868 x 1) x 0.15 = 1 681 rubles.- tax for one full month of IP.

If the activity is carried out completely on all calendar days of the quarter, then we multiply the calculated amount by 3 and get the amount payable = 5,044 (we round it according to the rules of mathematics).

If in a certain month the activity was not carried out or was not completely carried out, then we divide the number of worked calendar days by the total number of days in the month, and then multiply by the amount of tax for the full month.

For example, our IP started working on 05/04/2018. Then for the second quarter he:

• did not work in April (0 days);

• in May from 31 calendar days, worked out 28: 28/31 = 0.9;

• in June of 30 days worked out 30: 30/30 = 1.

The final calculation of UTII for IE for freight:

1681 x 0 + 1681 x 0.9 + 1681 x 1 = 3 194 rubles - the total amount payable for the 2nd quarter.

It is worth noting that to maintain this tax regime in their region, local authorities can reduce the tax rate to 7.5%. In the region from the example (Tolyatti), it is 15%.

How to legally reduce tax?

The amount payable to the budget may be reduced by:

• the entire amount of pension and insurance contributions to the individual entrepreneur himself paid during the quarter (if the entrepreneur is the only employee);

• no more than 50% of the estimated tax (subject to the availability of employees and payment of contributions to them to the FIU and the Social Insurance Fund for themselves and for themselves).

Even if the activity was not carried out for some periods, and according to the documents an individual entrepreneur was registered, payments to the UTII for freight transportation are transferred to the budget. On the one hand, this is a minus, because in case of difficulties with orders, the tax burden remains. On the one hand, it does not directly depend on the profit made, and may turn out to be significantly lower than monthly income.

Reporting and deadlines

How to calculate UTII for freight, we figured out. But it is also important not to forget that according to the results of the quarter, the entrepreneur must file a declaration with the control authorities and pay the tax. If there are no employees, then the individual entrepreneur submits reports according to a simplified scheme - only to the Federal Tax Service, and only a declaration of imputed income. Moreover, he does not have to register in telecommunication channels, but you can come in person and hand it over.

If there are employees, then in addition to tax authorities you need to visit the FIU and the FSS. Having assistants, IP is unlikely to do without an accountant, because paper and other work is increasing.

Reporting is important to submit before the 20th day of the month following the reporting. And you need to pay by the 25th of the month following the reporting one.

Maybe, at first glance, all this seems dreary and scary. But once you figure it out, you can save not only on the services of an accountant, but also on payments to the budget. And let your business prosper!