Often, in connection with the expansion of the scope of activity, the founders of the company decide to create a separate division. It involves the implementation of a number of organizational measures. Their volume will depend on the type of subsidiary. Further, the article will provide step-by-step instructions for creating a separate unit.

General information

The procedure in accordance with which the creation of a separate division is carried out, the model of the act adopted at the constituent assembly, the duties and rights of the main enterprise are regulated by civil law. A subsidiary may be a branch or representative office. There is a certain difference between them. The latter should be understood as the structure associated with the main enterprise, located outside the territory of its location. The creation of a separate unit of this type is carried out to represent the interests of the legal entity and ensure their protection. The branch is also located outside the territory of the main enterprise. However, this subsidiary structure carries out all its functions (or their specific part), including representation. These separate units must be indicated in the constituent documentation. This requirement is established by Art. 55 GK. In this regard, the creation of a separate division is allowed only with the introduction of appropriate changes to the local regulatory acts of the enterprise.

Important point

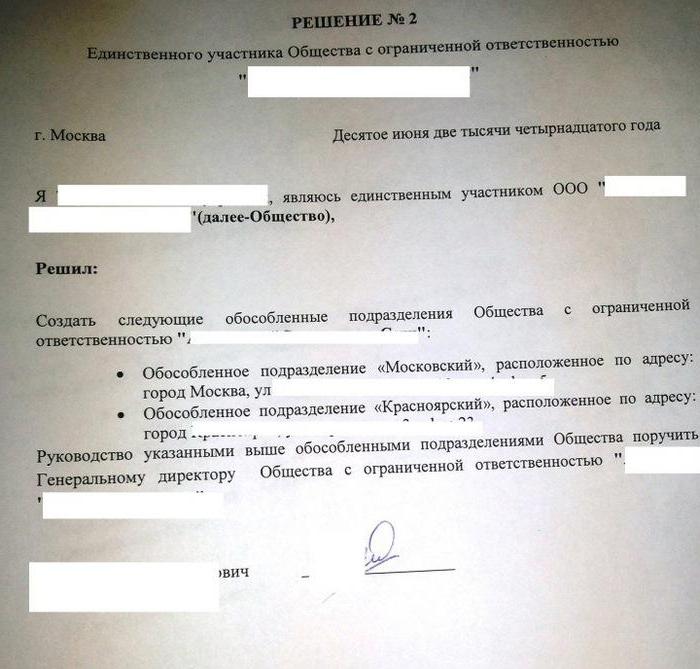

Amendments to the documentation are carried out by decision of the participants in the company or its competent executive body. Additions related to the formation of JSC subsidiaries, as well as their liquidation, are included in local acts by decision of the board of directors. The creation of a separate subdivision of LLC is within the competence of the meeting of participants. It is on it that the corresponding act is adopted, which serves as the basis for further necessary organizational and administrative measures. In accordance with the law, the changes made get legal force from the moment of their state registration. In some cases, for their entry into force, it is necessary to send a notice on the creation of a separate unit. It is provided to the authority performing state registration.

Design Features

The notice of the creation of a separate division must confirm that:

- Changes that are made to local acts comply with the requirements of the current legislation.

- Information of constituent and other securities are reliable.

- The procedure was followed in accordance with which it was decided to create a separate division.

A sample form of the notice on the formed subsidiary is given in Appendix No. 7 to government decree No. 439. Together with this paper, the company must provide sheet A (for the branch) or sheet B (for the representative office). The procedure in accordance with which the notice is issued is given in section VII of the methodological recommendations. Sheets A and B are filled out following the example of Forms D and E. The relevant rules are defined in Sec. III methodological recommendations.

Separate divisions: tax

The establishment of a representative office or branch is registered with the authorized body. The Federal Tax Service and its territorial structures act as him in the country.Having decided to create a separate unit (a sample of this act is present in the article), the legal entity sends certain papers to the Federal Tax Service. Their list is determined by law. It includes:

- Application for the creation of a separate unit. It must be signed by an authorized person of the enterprise.

- The decision to amend the local acts accordingly.

- Information about add-ons to be registered.

- A receipt confirming the payment of the fee.

Tax Code

The form on the creation of a separate division is provided not only in the Civil Code. The Tax Code defines the conditions for recognizing a subsidiary as such. A separate division is understood to mean any organization that is geographically separated from the main enterprise and whose location is equipped with fixed-type jobs (for a period exceeding 1 month). A subsidiary is recognized as such regardless of whether or not information about its formation is reflected in local acts. Nor do they have the meaning and authority with which it is vested.

reference

The NK does not define the concept of a workplace. In accordance with Art. 11, all terms, institutions of family, civil and other law that are used in the Code should be applied in the sense in which they are interpreted in other legislative acts. In this regard, to decipher the definition of a workplace, you need to contact the TC. According to Art. 209, the area where the employee should be located or where he should arrive to fulfill his professional duties is recognized as him. The workplace is indirectly or directly under the control of the employer.

Labor relations between the enterprise and the employee arise on the basis of a contract concluded between them. The parties to the agreement are the employer and the employee. An employee is a citizen who has entered into an appropriate relationship with the employer. The latter may, inter alia, be an organization (legal entity). Thus, a subdivision is territorially separated from the main enterprise, with stationary workplaces formed on it, where employees carry out their professional activities in accordance with the employment contract.

Arbitrage practice

Decisions often emphasize that the recognition of separate divisions of an enterprise is possible subject to the following conditions:

- Territorial office from the main enterprise.

- The presence of fixed-type jobs equipped outside the place of registration of the main organization and formed for a period of more than 1 month.

- Implementation of activities through this unit.

Registration

For tax control, payers are registered with the Federal Tax Service at the location:

- enterprises;

- separate unit;

- real estate and transport owned by the organization.

Legislation sets deadlines for registration. Papers must be submitted after an order has been issued to create a separate unit. A subsidiary should be registered within a month from the moment of its formation. The main company also has the obligation to inform in writing about all of its representative offices and branches operating in the Russian Federation.

Territorial office

Above were indicated the main features of separate units. Among them, one of the key is the territorial branch of the enterprise. The Tax Code does not disclose this concept. However, in accordance with the above art. 11 of the Code, you should contact the All-Russian classifier of units of administrative-territorial division. According to the provisions of the act, the isolation suggests that the location of the main company and the location of its subsidiaries do not match.According to the Ministry of Finance, a territorially separated structure should recognize a representative office or branch operating within a different area, different from the one in which the main organization operates. In other words, the creation of a separate unit is carried out at a different address than the one indicated in the constituent acts.

Nuance

If the order to create a separate subdivision involves the formation of a branch or representative office within the territory supervised by the same control structure as the main company, the subsidiary is not obliged to register with it. This follows from the provision that a payer who has registered with a specific authority in accordance with one of the established art. 83 reasons, you can not be held responsible for the failure to submit papers for a repeat procedure. This opinion is set forth in the decision of the Supreme Arbitration Court No. 5 of October 28, 2001. From this, in turn, it follows that the company may not send an application for registration of a separate subdivision to the Federal Tax Service if it is already registered in it due to the presence of a subordinate control body territory of transport or real estate owned by the payer.

Stationary jobs

Their formation is another prerequisite for the recognition of the unit as separate. It will be considered completed if at least two jobs are created or one employee performs activities in more than one position, specialty or qualification. However, in some court orders there is a different opinion. In particular, it is indicated that the unit will be considered isolated if at least one place for work has been created in it. This position is often used by employees of the Federal Tax Service. In one of the letters, in particular, the following was stated. In the clarification of the concept of a separate unit specified in Art. 11 of the Tax Code, the presence of equipped stationary places for work is one of its signs.

It should be borne in mind that this formulation absorbs the definition of a site for the performance of professional duties. In addition, the definition is given in the singular. This would be incorrect in semantic load if the legislator would not have recognized a unit that consists of one place for work. The authors of this letter also referred to one of the decisions of the FAS. It clearly established the need to register the creation of a separate unit. Documents are submitted in accordance with the decree, even if it is equipped with one place to work. Moreover, the rulings of the arbitration courts contain a rather important remark. The decisions repeatedly emphasized that the equipment of a place for work involves not only the formation of appropriate conditions for the performance of professional duties, but also the work itself.

Additionally

Evidence that the company has opened a subsidiary may be:

- Protocol on the creation of a separate unit.

- The lease agreement for the facility in which the company will operate.

- Employment contract with employees.

- Appointment Orders.

- Report card of work shifts and so on.

Legal responsibility

From the foregoing, it follows that having formed even one place of work in the territory controlled by another branch of the Federal Tax Service, the enterprise sends a statement no later than a month for registration at the location of its separate division. It is drawn up on the form f. No. 09-1-1. What else is needed to create a separate unit? In addition to the specified completed form, the company sends:

- A copy of St. va on registration of a legal entity with the Federal Tax Service at the location. She is notarized.

- Papers confirming the creation of a separate division.

The specified information shall be sent within a month from the date of formation of the subsidiary. In case of violation of the established procedure for registration with a legal entity, sanctions can be applied. They are established in Art. 116 Tax Code. In case of delay for a period not exceeding 90 days. after the end of the period allotted by law, the organization is charged with a fine of 5 thousand rubles, if the delay is more - 10 thousand rubles. In addition, fines of up to 1 thousand rubles may be exacted from company officials. If a separate division carries out activities without registration, then this can be regarded by the control authority as an evasion of accounting. This violation shall entail a penalty, the amount of which amounts to 10% of the profits earned by the subsidiary. The amount of the fine may not be less than 20 thousand rubles. In the case of activities without registration for more than 3 months., Sanctions increase to 20% of income.

Controversial situations

The above provision regarding the timing seems to many entities not specific. This, in turn, causes ambiguity in understanding the norms. In most cases, employees of the Federal Tax Service consider that the calculation of the term starts from the moment a decision is taken to form a unit. However, as indicated above, as a mandatory feature for recognizing an enterprise as geographically separate, is the equipment of a place for work. Only a small number of payers at the time of making the appropriate decision does it exist. The remaining entities need time for their equipment. Attempts by the control services to use the date of adoption of the relevant decision as a starting point for calculating the deadline for imposing fines are not always supported by arbitration courts. As an argument, reinforcing the position of the Federal Tax Service, acts on the completion of work on equipping the workplace.

As for the lease, it, in the opinion of the judges, cannot be unambiguous evidence of the formation of sections at the enterprise for employees to fulfill professional duties. It does not indicate the creation of a workplace and the signing of a contract with an official, accrual and payment of his salary. In some cases, this opinion is supported by the Ministry of Finance. In particular, when entering into appropriate relations with a citizen who conducts his business by searching for information through electronic means of communication (via Internet channels or at home) or in libraries without creating a stationary type of workplace for him, it cannot be considered that the enterprise has formed a separate subdivision. In this case, the place of residence of the individual does not matter. At the same time, the conduct of certain economic activities by an enterprise in a territory that differs from the address given in the constituent acts is considered to be carried out through its separate division.

Interaction with funds

For legal entities, there is a certain procedure for registration with extra-budgetary government agencies. In particular, it is made on the basis of data present in the register. They are transferred by the FTS to the respective funds. When creating separate units, these rules do not apply. Insurers need to register on their own at subsidiaries. it done in:

- Territorial MHIF.

- Executive structures of the FSS.

For registration is given a month. The calculation of the term is carried out from the date of creation of the unit. Moreover, the legislation provides an important explanation. Registration in the FSS is carried out by those units that have a separate balance sheet, payroll and charge payments and other remuneration in favor of citizens. The procedure is carried out in accordance with the appeal of the interested subject.The application form is given in Appendix No. 1 to the Rules for the registration of policyholders in the territorial MHIF.

FIU

Article 11 of the Federal Law No. 167 does not establish the obligation to register with insurance companies in the territorial structures of the Pension Fund. Meanwhile, mention of it is present in the Procedure approved by the PFR board. Registration of insurers at the location of separate divisions, which have a separate balance sheet, payroll and accrue fees and other payments to citizens, is carried out when they apply to the Fund. The procedure is carried out on the basis of information present in the Unified State Register of Legal Entities and forwarded by the Federal Tax Service to the FIU. When the company is registered in the territorial structure of the Pension Fund as an insured, the notice in duplicate is sent to the address of the location of the separate subdivision. One of them is submitted to the fund body within ten days.