Each person planning the registration of an individual entrepreneur or company thinks about which tax system to choose. It is depending on the chosen regime that determines how many taxes the organization will pay, as well as what benefits and concessions from the state it can use. At the same time, entrepreneurs often think about what OSHO is. This system is represented by the general mode, which can be used by both individual entrepreneurs and companies. It is the most complex, since it is mandatory to keep accounting records, and numerous fees are calculated and paid.

The concept of basic

When studying the numerous taxation systems that entrepreneurs in Russia can use, many people want to know what the basic taxation system is. The features of this tax regime include:

- automatically all new companies or entrepreneurs are transferred to this system if within 10 days after registration they do not submit a notification to the Federal Tax Service about the transition to another mode;

- usually selected by the OSNO by companies and entrepreneurs who need to use VAT to work with different suppliers or customers;

- when choosing this mode, it is important to prepare for the need to pay numerous fees, as well as for conducting complex accounting;

- the main fee in this mode is income tax, showing the result of the company.

It is allowed to combine the general regime with other tax regimes permitted in the Russian Federation. An exception is the use of OSNO at the same time as the simplified tax system or the unified data storage system.

Difference from other systems

To understand what OSNO is, it is important to understand the differences between this mode and other systems. These differences include:

- simplified regimes are applied exclusively by taxpayers, suitable for different requirements related to the number of employees, profit or fixed assets, but the general system can be used by any company or individual entrepreneur without restrictions;

- when using preferential systems, the tax burden is significantly reduced, but when applying the OSHO it is important to prepare for the need to calculate and pay a huge amount of taxes;

- necessarily all companies on the OSNO pay property tax to the budget.

Income tax is paid exclusively when using the general regime. When using other systems, only one tax is calculated, replacing several taxes represented by income tax, VAT and property tax.

When is it profitable to use OSNO?

If you are well versed in all the features of OSNO, then using this mode is actually beneficial. It is recommended to choose it under the following conditions:

- the main contractors use OSNO, therefore they pay and reimburse VAT;

- the company’s activities are connected with the external economy of the country, therefore it is advisable to apply a regime if the company sells goods to foreign countries or imports goods across the border into the territory of Russia;

- the company selects activities that fall under the income tax exemption, for example, engaged in agriculture, works in the field of medicine or provides social services to the population.

In the above situations, the choice of OSNO is the best solution. At the same time, the OSNO accounting policy is independently selected and established by the head of the company.

Pros and cons of using the system

To understand what OSNO is, and also when it is advisable to use the mode, it is recommended to study the positive parameters of the system application well. These include:

- the main plus is the payment of VAT, since when calculating this fee, you can attract a large number of large counterparties who work under the general regime, since this interaction allows you to reduce the tax burden;

- there are no restrictions for entrepreneurs, so you can work in any direction of activity, increasing revenue and profits;

- Entrepreneurs can combine OCHN with UTII or the patent system, which provides the opportunity to optimize taxation.

The disadvantages of applying the general regime include the need to calculate and pay a large number of different fees. Be sure to use the help of a professional accountant during the start of work, since annually a large number of reports, declarations and other documents are required to be prepared.

The nuances of using OSNO companies

Most commonly used by OSNO organizations. This mode is chosen by representatives of large business. With revenue that exceeds 150 million rubles per year, it will not be possible to use various simplified systems. The features of the use of OSNO by different companies include:

- enterprises are payers of income tax, and the rate for this collection is 20% of the profit;

- income tax is paid quarterly or monthly;

- VAT must be calculated if the income received does not provide an opportunity to obtain exemption from payment of this fee;

- firms transfer insurance payments for all hired specialists, therefore 26% are transferred to the PF, 2.9% to the Social Insurance Fund, and 5.1% of each employee’s earnings to the FFOMS;

- in accounting, the accrual method is used to calculate fees, but it is allowed to use the cash method with a small income;

- large taxpayers are required to maintain full accounting, so simplified accounting is allowed exclusively for small companies.

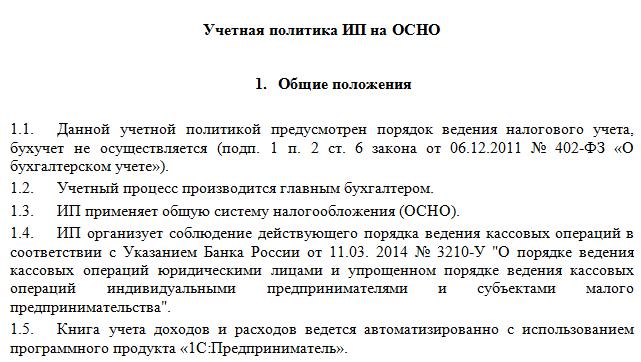

The peculiarities of using the general regime are the need to maintain an accounting policy on the OSNA. A sample of it can be studied below. The process is performed by both firms and individual entrepreneurs.

Specificity for IP

The transition to OSNO is allowed not only for companies, but also for private entrepreneurs. The use of this IP mode has the following features:

- the main tax for entrepreneurs is personal income tax, which makes up 13% of the income of individual entrepreneurs;

- the number of reports and declarations drawn up by the entrepreneur compared with companies is reduced;

- When working in any mode, an individual entrepreneur is obliged to transfer fixed payments to state funds for himself.

Typically, entrepreneurs prefer to use simplified modes, which significantly reduces the tax burden. With preferential systems, usually one declaration is submitted, which the individual entrepreneur can draw up. If OSNO is selected, then accounting is much more complicated, therefore it is advisable to immediately hire a professional accountant.

Transition Rules

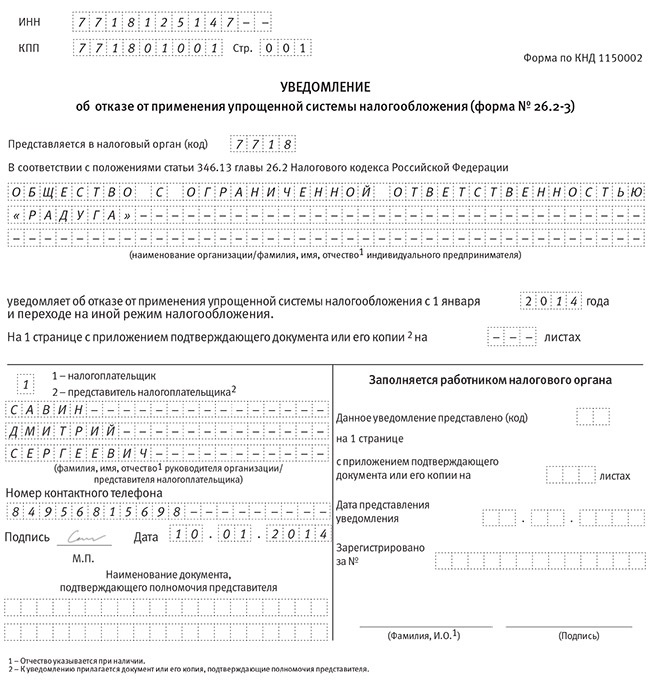

If the individual entrepreneur or the head of the company decides to use the general regime, the question arises of how to switch from the simplified tax system to the basic taxation system. The procedure can be performed in various ways:

- if the registration of a company or individual entrepreneur is carried out, then all taxpayers are automatically transferred to the OSNO, therefore, if you do not submit a notice of transition to another regime to the Federal Tax Service within 10 days, you can use the general regime;

- in order to switch from another regime, it is enough to submit at the beginning of the year a notice of withdrawal from the privileged system;

- if a company or individual entrepreneur ceases to fit the requirements of a simplified system, it automatically switches to general mode.

Most often, entrepreneurs switch to OSNO in violation of the requirements for the use of simplified modes.For example, their revenue may increase to 150 million rubles. more than 100 people are registered per year or in the staff. If UTII is used, then it is likely that at a certain point in time the local authorities of a certain region will prohibit the use of this regime.

For the transition, it is not necessary to draw up an application for OCO, as it is enough to draw up a notice of termination of activity for the previously selected simplified regime.

What reports are compiled by companies?

If firms choose the general regime, the following types of documents are prepared regularly:

- VAT returns are drawn up once a quarter, and the fee itself is transferred every month;

- income tax report formed quarterly and surrendered by the 28th day of the month following the reporting quarter;

- financial statements presented by the profit and loss statement and balance sheet, moreover, these documents are submitted before April 1;

- transport tax declaration;

- property tax report, which takes into account which objects of taxation are used for the business of the company.

If the company suspends work at a certain point in time, then it is allowed to draw up and submit zero declarations. At ESSA, reporting may be submitted electronically or in writing. In the first case, digital signature is required.

Reporting for IE

Entrepreneurs must compile the following types of reports on the OSNO:

- VAT return;

- 3-NDFL declarations for the employer are drawn up once a year, moreover, if the head is a resident of the Russian Federation, 13% will be charged on his income, and if he is a non-resident, 30% will be charged;

- if the cadastral value is calculated for the property used in the process of work, then property tax is paid for it, therefore, a declaration is annually drawn up for this collection.

Additionally, firms and entrepreneurs prepare various licenses and permits for the chosen area of work. If they hire specialists, then you have to pay for all citizens contributions to the Federal Tax Service and various state funds. A report is prepared before April 1 of each year for employees, and 6-NDFL declarations are also submitted. Special documents are transferred to the PF and other state funds.

Combination with other modes

It is allowed to combine the taxation system of the special taxation system with other regimes, but the exception is the USCH and the simplified tax system. Therefore, the most common common mode is used in conjunction with UTII.

When using various systems, it is important to know about the rules for maintaining separate accounting. For each tax, income and expenses are calculated. If some costs are applied to two systems, they are allocated when taking into account the selected activities.

Conclusion

OSNO is a general regime that can be applied by both IP and various companies. Using this system has many advantages and some disadvantages. There are some situations where the use of OSNO is most beneficial for taxpayers.

If companies or individual entrepreneurs choose the general regime, then they should understand what taxes have to be paid, as well as which reports are prepared by the Federal Tax Service. If you violate the requirements of tax laws, you will have to face serious fines.