CPM - a very important indicator when applying for a loan. This abbreviation stands for the total cost of the loan. What it is? How is this indicator calculated? What is included in it? How to calculate it yourself? Is it possible to get accurate results? These and related issues can be found in the article.

What is it?

The total cost of the loan (CPM) is an information indicator by which it is possible to compare loan offers from various banks and MFIs (microfinance organizations). This is very valuable data, because with the help of CPM you will determine which loan will be less costly for you.

This value is calculated as a percentage (%). But in December 2017, the Consumer Loans Act was amended. According to them, the calculation of the total cost of the loan should be made not only in percent, but also in monetary terms.

In fact, everything is clear. If a loan is given, say, at 20% per annum, then it turns out that you will overpay 20% of the loan amount annually. But the borrower pays much more than indicated in an attractive rate.

The fact is that the value of the full cost of a loan is not always indicated by banks in advertising offers, only in loan agreements. And borrowers find these mostly unfavorable conditions for them after signing the document.

Market average

Now let's move on to the statistics. According to the Central Bank of Russia, the total cost of loans, consumer and automobile, is expressed by the average market value in the range of 13.7-26.8%.

Market average for MFIs

As for MFIs (organizations issuing microloans), the indicators here are slightly higher. Sometimes they even reach fantastic numbers. For example, for an unsecured microloan in the amount of up to 30 thousand rubles, drawn up for one month, the average market full cost of a loan can reach up to 600%!

Accordingly, the more the volume and term of a loan from an MFI increases, the more this value will approach banking. So, if an unsecured microloan is issued for a period of about a year, and its size exceeds 100 thousand rubles, then the average market value in its ratio is 32.5%, and the limit is 43.4%.

Now we will examine whether the value of the total cost of a consumer loan is equivalent to the advertised rate. Consider what banks are required by law to include in the CPM for settlements, and what not.

What is included in the CPM?

We continue to analyze the full cost of the loan. What it is? These are all loan payments that are known at the time of the conclusion of the loan agreement.

Consider them:

- Main debt. This is the main value in the formula proposed by law. But she is far from the only one. In addition to it, there are many quantities that are paid by the borrower in excess of repayment of the main debt.

- Interest on the loan. That's it they are the advertised bid.But at the same time, interest on the loan is far from the only thing that remains to be paid to the borrower.

- Payments to the bank. Only those payments are indicated here, without which the issuance of a loan is not possible. For example, if a loan is issued for an apartment, a fee may be necessary for placing a decent decent amount of cash in an individual safe.

- The cost of issuing a credit card. Provided that the funds will be credited to it, and not issued in cash.

- Payments to certain third parties, if the provision of a loan depends on the contract with them. Such persons, of course, must be indicated in the contract. Most often, they are the insurer, notary or appraiser. A fee means insurance premiums, payments for the assessment of collateral, transfers of funds to accounts of other banks, etc.

- The cost of insurance. For those cases when compensation for an insured event is paid not to the borrower, not to his relatives. So, in the structure of the CPM, the cost of life insurance will be taken into account if, as a result of the death of the borrower, it is the bank that receives compensation for repaying the loan with these funds.

- Insurance determining the conditions of the loan. These are insurance contracts that determine the amount, terms, interest rates when applying for a loan. Many banks raise interest rates on loans if the borrower does not draw up an insurance contract. In such cases, insurance purchased by the credited must be taken into account when calculating the total cost of a consumer loan, loan.

Exceptions when calculating payments to third parties

Now about the exceptions. “Payments to third parties” do not include collateral insurance (for example, comprehensive insurance when applying for a car loan). Amendments to the law, adopted in December 2017, oblige to take into account when calculating the full cost of a consumer loan, real estate insurance mortgage loan.

Moreover, if the name of the organization is written in the loan agreement, then the calculation will be made at its rates. If the bank does not limit the range of insurers that the client can contact, use the tariffs of any of the insurance organizations. Therefore, in this case, the UCS calculations will be only approximate.

But the bank here must definitely specify at the rates of which insurance company it makes the calculation. In this case, the contract should state that when choosing another insurer, the insurance company may be different.

It is important to remember that when calculating payments to third parties as part of the CPM, banking specialists use insurance rates that are current at the moment. From this we cannot exclude the possibility that in the future these tariffs will change and the cost of payments will increase / decrease.

What is not taken into account in CPM?

Above, we presented the average market value of the total cost of the loan. And now what is not taken into account in the calculation of UCS:

- Payments required by law. For example, CTP when applying for a car loan.

- Payments resulting from a breach by the borrower of the terms of the contract. The most common example is late payment penalty. This is quite logical, since it is impossible to predict the probability of such violations in advance.

- Payments that depend directly on the decision of the borrower. First of all, they should be associated with the loan itself and the contract. For example, making an early payment fee.

- The cost of collateral insurance. Most often they are hull.

- Insurance.

Insurance issue

As for the last of the above list, then when calculating the total cost of the loan, the Central Bank determines the following conditions under which the cost of insurance is not included in the CPM:

- The execution of the insurance contract does not affect either the size of the loan, or the very possibility of providing a loan.

- When making such a service, the borrower receives some additional benefit for himself.

- A so-called cooling period is valid for 14 days. That is, without consequences for themselves at this time, the borrower can refuse insurance services.

Simple loan calculator

Sometimes the borrower needs to calculate the CPM on his own. The best way here is to use an online loan calculator. Such an option, besides free, offers a lot of Internet resources.

You only need to enter data from your payment schedule into the required fields. If you have not yet entered into a loan, then you will have to look for the necessary information on the website of the bank that interests you.

The simplest version of the calculator contains the following graphs:

- Credit amount.

- Interest rate.

- Loan terms.

- One-time commission.

- Monthly commission.

- Payment type.

- Start payouts.

The result in most cases is not in percent, but in rubles. However, the calculations will be approximate.

Sophisticated loan calculator

To get a more accurate result, you need to find a more detailed online calculator. For example, a result close enough to reality can be obtained by filling out the following parameters:

- Type of payment.

- Loan amount.

- Loan interest rate.

- Loan terms.

- Beginning of loan repayments.

- Insurance.

- All standing commissions.

- Cost of evaluation.

- Interest rate reduction fee.

- Bank cell rental.

- Other one-time banking commissions.

Calculations in the EXCEL program

An alternative to an online calculator is a popular office program. Open the standard table and proceed according to the following algorithm:

- In column B, enter all payment dates. Zero (first in the list) here will be the date of approval of the loan. It is on it that the calculation (discounting) is made - the determination of the value of the UCS.

- Column C contains all amounts paid by the borrower. Please note that the first of them will be negative - this is the size of the approved loan. All subsequent ones are positive. These are the payments you make according to your schedule.

- You will need the IRR function. In this case, it is equivalent to UCS. Its name is "PURE".

- To make calculations in the last cell in column C, put an equal sign.

- Then enter the name of the formula - “PURE”.

- Put a bracket and enter all the values from column C (just click in order on the filled cells).

- Put a semicolon.

- In the same way, list all the values from column B.

- Remember to close the bracket.

- After that, press “Enter” (Enter key).

If you did everything correctly, in the last cell of column C you will get the desired number. It is expressed not in percent but in fractions of a unit. For example, 0.3401. To return this value to a percentage, just multiply by one hundred. In our case, the value of UCS will be equal to 34%. That is how much you overpay on your loan.

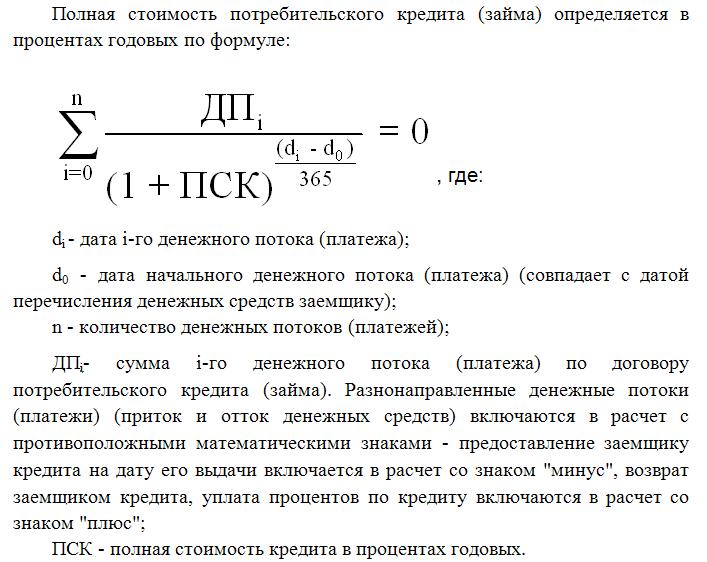

Calculation using the formula

The most difficult way is to use the formula that the Federal Law on Consumer Loans offers. You will see it later in the article. Of course, the calculations here will be the most accurate, but in this case you cannot do without knowledge of financial mathematics. By the way, it is this formula that banking specialists use when calculating CPM.

The full cost of the loan here corresponds to the internal rate of return indicator (IRR in financial mathematics). This value is equal to the interest rate at which the discounted net income is zero.

The net income of the bank in general is the amount that the client overpays. Discount here is the reduction of future money to its present value. Accordingly, all loan payments are discounted to the date of issue. Hence, the net present value is the total amount of all discounted payments by the borrower.

CPM is a very important value for the borrower. As you have seen, it differs from the interest rate on bank brochures, moreover, to a greater extent. Calculating the CPM means accurately determining how much you will overpay by repaying the loan.