Every law-abiding taxpayer has a legal right to a VAT refund. The procedure is prescribed in the Tax Code, in particular in Article 78. You can rely on tax refunds if, at the end of the reporting period, the person who declared their income has a deduction that exceeds the amount of VAT charged.

VAT refund allows legal entities to rationally use their own assets and even increase competitiveness.

Guarantees

Most often, situations in which a tax refund is possible arise for exporting enterprises that operate at a 0% rate (this rule is enshrined in article 165). However, the fact of exceeding the amount of deductions is not a reason for a tax refund. To get under this procedure, you will have to fulfill a number of requirements provided by applicable law.

The first condition of the VAT refund procedure for legal entities is a desk audit of the Federal Tax Service. If we are talking about exporters, then in the verification process they will have to provide a fairly voluminous package of documents that will confirm two facts:

- the right to apply a 0% sales rate;

- justifications giving the right to the deduction amount.

Therefore, it is very important that every step of the transaction is correctly documented.

Legal entities entitled to VAT refunds

VAT refunds for legal entities are provided for by the Tax Code of the country, in particular article 176. In order to receive refunds, an enterprise should meet a number of requirements:

- be a payer of value added tax;

- services or goods for which an overpayment has arisen should be acquired exclusively for entrepreneurial activity;

- must be present invoices for this product indicating the amount of VAT, the signature of the chief accountant and the head of the enterprise;

- acquired material values or services must be capitalized;

- The transaction on which the VAT refund is supposed to be real;

- the seller and the buyer must have documents in full order, they must be registered in the manner prescribed by law.

VAT refunds are not allowed if the company is in the simplified tax system, unified industrial tax system or other tax regimes. The applicant must be listed as a VAT payer.

Possible tax refund options

VAT refunds for legal entities can be carried out in two forms:

- by offset;

- by return.

The first option assumes that the applicant has arrears in paying other taxes or there are outstanding fines or penalties. In this case, the tax office sets off the mutual claims on its own. If funds are left after the arrears are paid, they are returned directly to the taxpayer. Also, the taxpayer has the right to file an application so that the overpaid amount is sent to account for future payments of federal taxes, including VAT.

Refund of excessively paid tax is possible only subject to compliance with all legal norms of the enterprise and in the absence of debts.

Return Scheme

What is VAT? How can it be returned? For a complete understanding of the whole procedure, a tax refund scheme can be represented in several stages.

It should be understood that VAT refunds are not an automatic procedure. The interested taxpayer is obliged to independently initiate the procedure for the return of excessively paid tax.

Step No. 1 - filing a declaration showing the amount of VAT presented for refund

IFTS employees are required to conduct a desk audit (which lasts 3 months) of the submitted declaration. At this stage, tax officials are entitled to request from the declarant any documents that confirm the possibility of applying tax deductions. This norm is enshrined in article 88 of the Tax Code.

In cases of non-detection of any violations, you can immediately proceed to step number 6, that is, the tax authorities decide on the tax return and reimburse the overpaid amount.

Step number 2 - act to identify violations

How to return VAT to legal entities? If during the desk audit violations were found in the preparation of the declaration, then until they are corrected, deductions cannot be obtained until the deficiencies are eliminated.

The tax authority that conducted the audit makes a decision and reflects what deficiencies should be addressed.

Step # 3 - Objections

The taxpayer within a month after receiving the audit certificate has the opportunity to file their objections to the decision. This norm is enshrined in article 100, however, when submitting a protest, one should justify one’s position and point out the revealed violations in the actions of tax service specialists.

Step # 4 - Tax Response

The methods and procedure for VAT refunds for legal entities suggest that after filing an objection (or in their absence), the tax service experts make a decision after 10 working days. It may contain information about the involvement or refusal to bring the declarant to administrative responsibility. The tax service is obliged to notify the taxpayer of the decision made within 5 days from the date of such a decision.

In addition to being held accountable, if serious violations are found that are not resolved within the time period established by law, the taxpayer is refused a tax refund.

If there are no violations, then before making a positive decision, employees of the Federal Tax Service find out the issues of arrears of VAT, other taxes, fines and penalties.

Step number 5 - offset

If in the process of checking tax arrears the fact of its existence is nevertheless revealed, then the tax service specialists independently set off against the repayment of the existing debt. If the arrears were formed during the period when the inspection was carried out, then a penalty is not charged on it.

In cases where the tax return is not enough to pay off the arrears, the taxpayer is obliged to pay extra.

Step number 6 - making a decision on VAT refunds and tax refunds

How is VAT refunded? The return scheme to legal entities involves a further step in the form of a decision of the IFTS on VAT refunds. Such a decision shall be made if during the desk audit no violations were revealed or after the arrears, fines and penalties were paid, the amount to be paid remained.

After the relevant decision is made, the IFTS authorities send the corresponding order to the OFC (Article 176 of the Tax Code).

The tax must be transferred to the taxpayer's current account within 5 banking days from the date of receipt of the notification by the OFK bodies, which, in turn, is obliged to inform the tax service about the transfer of funds.

In cases where there are no violations in the procedure, it is considered fully completed.

Step No. 7 - violation by the FTS authorities of the terms for VAT refunds

How to return VAT to legal entities? It may happen that there are no violations on the part of the taxpayer, but the tax service still violated the terms of the tax refund. What to do in this case?

The declarant has the right to demand the calculation of interest on the amount to be returned. This right arises from the taxpayer on the 12th day after the decision on completion of the desk audit and the adoption of the decision on compensation.

How to increase your chances?

It is not at all difficult to collect documents for VAT refunds for legal entities, to observe the rules of the procedure, however, in practice, quite often, tax service specialists do everything to find violations and not refund the funds.

To increase your chances of tax refund, first of all, you should choose decent counterparties and follow the rules of paperwork, namely:

- keep records of services and goods in all journals provided for by regulatory enactments;

- do not forget to put a mark on the passage of customs;

- check whether all goods are VAT included;

- Check if all invoices are in stock and if all goods are included there;

- Be sure to pay VAT at the border when selling goods outside the country.

What documents need to be prepared

What documents are needed for submission to the IFTS during a desk audit? How to return VAT to legal entities? If the company is confident that its business activities are carried out within the framework of the current legislation, and there are no violations, then you can safely submit documents for tax refunds.

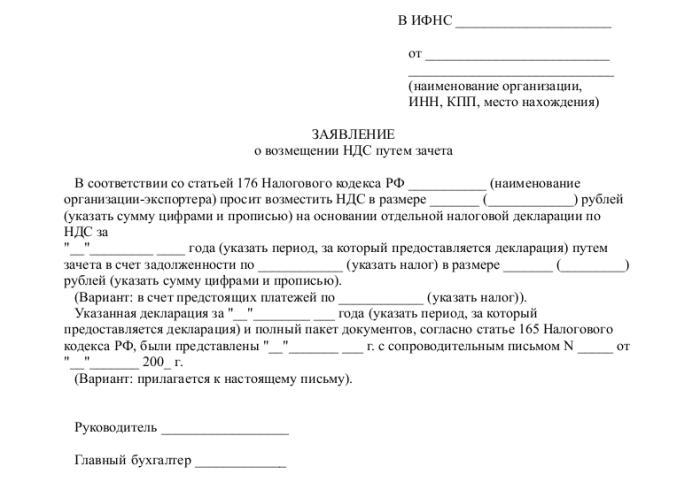

To initiate the procedure, prepare and submit a specific list of documents:

- application in the prescribed form;

- tax return for the relevant reporting period;

- a letter in which to request a refund of VAT;

- invoices;

- extracts from books of sales and purchases;

- other payment documents (for export operations - customs documents).

At the time of filing the documents, the company should not have debts: the lease debt should be repaid, all bills paid, that is, there should be no claims against the legal entity.

Conclusion

How to return VAT to legal entities? In principle, this is not a complicated procedure, but it requires special care and scrupulousness in the work of an accountant at each stage of the acquisition, sale of goods or services.

If, during a desk audit, IFTS specialists still found any inaccuracies, then all clarifications and explanations should be submitted exclusively in electronic format on the TCS. Otherwise, according to Article 88 of the Tax Code, such explanations will not be considered provided.

It should also be remembered that despite the right of the Federal Tax Service Inspectorate to request documents in the course of a desk audit, nevertheless, these requests should relate to the verified declaration. For example, the tax authorities are not entitled, checking the declaration, to be interested in the issue of low wages of employees or to demand explanations about the existence of losses.

And you should always remember that in case of disagreement of the taxpayer with the conclusions of the tax service and in case of refusal of compensation, the declarant has 90 days to appeal such a decision (from the moment of its adoption).