Accounting policy is an important document binding on each organization. However, one should know what kind of exemptions can be expected from this side if a person registers himself as an individual entrepreneur. What is the accounting policy of IP on the STS "Revenues", we will consider in this article.

Individual Entrepreneur Status

Registration of IP imposes certain obligations on the businessman. This is the submission of declarations to the tax, reports to various budget and extra-budgetary funds, the notification of the start of business, accounting. IP is obliged in its activities to follow the adopted tax system. In accordance with this, he must make payments to the budget.

How to calculate taxes

Taxation of individual entrepreneurs, as well as legal entities, is carried out in accordance with applicable law. Currently, in Russia you can choose one of five modes and follow it when calculating taxes:

- The simplified tax system (STS) involves only a small part of the documents for reporting. IP on the USN without workers, if not used for business, is the most suitable and simple way. The tax is calculated at a rate of 6% of income.

- The Unified Agricultural Tax (UPC), the name of which speaks for itself, allows payment of 6% of the difference in income and expenses.

- The patent tax system (POS) determines the payment of a fee equal to the value of the patent, and the possibility of doing business without cash register.

- The single imputed income tax (UTII) implies the payment of 15% of the rate approved by law. It doesn’t matter if the businessman has employees or does he conduct business without employees. Reporting IP to the STS for most businessmen is a more appropriate solution, since at UTII payment of taxes is carried out even in case of loss.

- General taxation system (OSNO) is quite complicated for layperson. It requires the businessman to conduct serious accounting. The individual entrepreneur will be forced to use the services of an accountant or a specialized company that will help him in reporting and calculating taxes.

What you need to know about accounting policies

IE on the simplified accounting system “Revenues”, in spite of the so-called simplified accounting, is not exempted from obligations on the formation of accounting policies. Such a document must be created by a businessman within 90 days from the date of registration. According to its provisions, the activities of the entrepreneur are carried out.

How to compose a document

It should be noted that the structure of accounting policies in simplified accounting is quite primitive and includes two large sections: tax and accounting.

As for tax accounting, the entrepreneur cannot use any individual calculation methods. That is why the main provisions of the Tax Code should be reflected in this part. In relation to the second section, it is necessary to be guided by Federal Law No. 402-ФЗ “On Accounting” and Regulation on Accounting PBU 1/2008 “Accounting Policy of an Organization”.

Since the law clearly defines whether an IP accounting policy for USN is needed, it is imperative to delve into the meaning of the Federal Law and Accounting Regulations regarding the necessary items and draw up your document for future use.

Tax accounting

When simplified taxation of individual entrepreneurs in the accounting policy should reflect:

- Tax object and tax rate.

- The composition of revenues, the way they are accounted for and how it is maintained (manual recordings or electronic generation of KUDiR).

- Possible reduction of the base from which tax is paid by the amount of insurance premiums.

- A way to adjust the amounts in the current period for errors in past reports.

- Responsible persons.

Good example

IE on the simplified tax system "Revenues" may draw up a document to ensure competent tax accounting, containing the following items:

- Tax accounting is maintained by an individual entrepreneur (full name).

- IP (full name) applies a simplified taxation system. When calculating the amount of tax for the object of taxation, income is accepted based on Article 346.16 of the Tax Code of the Russian Federation.

- In order to determine the tax base, data from KUDiR are used. For the individual entrepreneur on the USN (full name), the necessary calculation is carried out in manual mode based on the primary documents. Ground of decision: Art. 346.15 and 346.24 of the Tax Code.

- The calculation of the tax amount is carried out taking into account the reduction in the amount of payment due to the amounts of compulsory insurance.

If suddenly two tax systems are applied in parallel for different types of activities, then it is additionally necessary to reflect this information and carry out separate accounting.

Accounting

The accounting policy of FE on the STS “Revenues” in terms of accounting has no differences from its design by businessmen and organizations located in other regimes. The basic requirements for compiling this document include the following points:

- Maintenance is carried out on the basis of Federal Law No. 402-FZ and PBU.

- In accounting, the chart of accounts approved by Order No. 94n of 10/31/2000 is used.

- Responsible for the accounting policy of the individual entrepreneur on the simplified tax system “Revenues” and conducting accounting is an entrepreneur indicating his name and surname.

- Unified forms of primary documents are used (must be listed).

- Used manual (or automated) management BU.

- The possibility of adjusting accounting errors of past periods in the reporting period and the ways of these corrections are indicated.

- In the case of production, methods for evaluating the initial goods and materials used in the manufacture of products are reflected.

- The procedure for recording income and expenses is described (if the STS “Income minus expenses” is used).

Ledger

According to the requirements of the law, it is now mandatory for a businessman to comply with the requirement to maintain a KUDiR for individual entrepreneurs on the simplified tax system. We will understand what this abbreviation means and how to work without violating the rules for maintaining this document.

The IP book is mandatory to fill in the book of income and expenses if he has chosen a simplified taxation system for himself. This document in chronological order reflects all business transactions. This means that it records all the income of the merchant and his expenses on entrepreneurial activity.

It should be noted here that it is mandatory to maintain such a document only for businessmen who are on simplified business and basic educational programs. In other cases, the book of accounting for income and expenses of IP is not needed.

Book Design Rules

Legislation allows both paper and electronic versions of the document.

The electronic version is easier to make corrections if errors are found. However, it is not forbidden to correct the detected errors in the manual version, only confirm them with the signature of the entrepreneur, his seal and the date of entry. At the end of the reporting period, the book should be kept for another four years. Submit KUDiR to the tax should only be requested by the inspector. Together with the submission of the declaration, the USN IP should not present the book. Before transferring to the tax on demand, if you kept computer records, it is necessary to check that KUDiR is flashed, numbered, and on the last sheet there was an IP seal with its signature. If you fill out the book manually, then the firmware and other manipulations must be done at the very beginning of the tax period.

It should be borne in mind that for each amount that is deposited in KUDiR, the entrepreneur must have confirmation. The first entry should reflect the first income or expense in the current tax period.

KUDiR must be completed in Russian. If the primary document confirming the expenses is executed in a foreign language, its translation is required. The expenses and income reflected in the book can be recorded only in rubles. The amount spent on the purchase in another currency must be converted at the rate of the Central Bank of the Russian Federation on the day of purchase and entered in the corresponding line only in rubles.

How to fill KUDiR

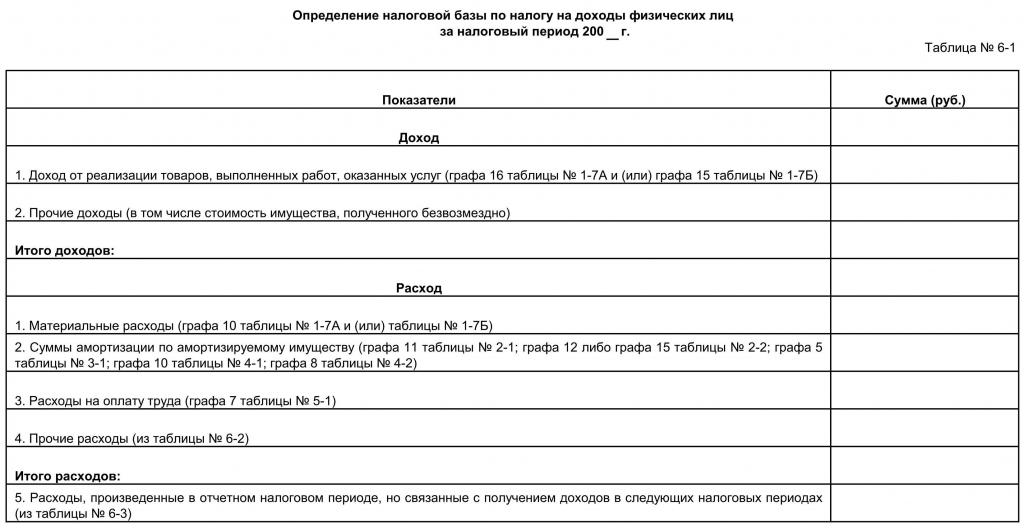

For the reporting period, the year or those months when the entrepreneur received his status is taken. If this happened, for example, in the second quarter, then the book begins to lead from this time. For each quarter, it is necessary to allocate a separate section. Data for the first quarter should be in the first section, the second should include figures for April, May, June and a total of six months, the third should reflect the amounts for July, August, September, as well as expenses and income for nine months, the fourth should be entered figures for October, November, December and annual.

On each page should be the number of the operation, its essence, date and number of the supporting document and the amount thereon.

A businessman should know the following:

- The book records only those expenses and incomes that are involved in the calculation of taxes, that is, those for which primary documents are available.

- If the STS "Revenues" is selected, then it is allowed not to enter the expenses in the book, but only indicate the income.

What reporting does an entrepreneur give on simplified

The law provides for the delivery of IP declarations to the USN once per period. The term is limited to April 30 of the year following the reporting year. Filing later than the specified date is punishable by a fine. At the same time, you should be aware that advance tax payments must be made every quarter at the rate of 6% of the received income in the previous quarter in the case of the STS “Revenues” and 15% for the STS “Revenues minus expenses”.

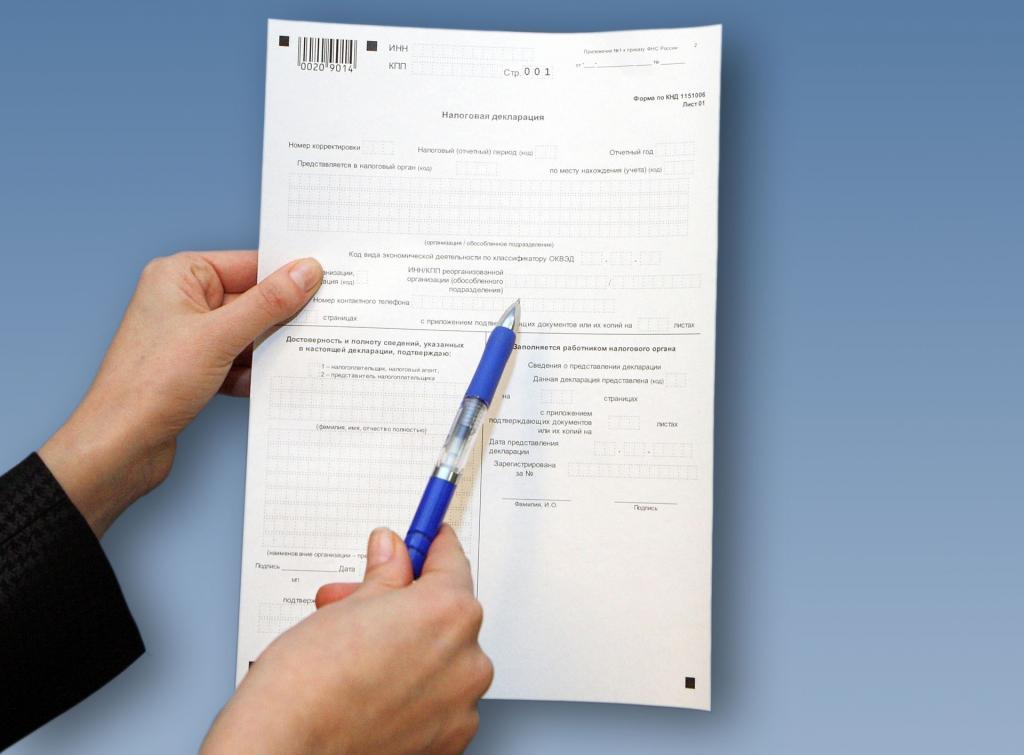

For self-completion of a declaration by an entrepreneur at the STS “Revenues” study the following recommendations:

- Three sheets must be submitted: title page, section 1.1, section 2.1.1.

- On each sheet is stamped TIN.

- The page number is indicated on the 2nd and 3rd sheet.

- On the title (first) sheet, fill in the correction number (0 - if the document is first submitted, 1 - if the second time after detecting errors); tax period code (34 - means that the declaration reflects information for the year); reporting year; tax code and location code; Name, OKVED, phone number; the number of sheets and the number "1" in the field "Taxpayer / taxpayer representative".

- Next, the third page is filled out, where it is indicated on an accrual basis (that is, for three months, then for six months, then for nine months and for one year) income, tax rate, tax amount and the amount by which it is reduced.

- Now the values on the second page are put down, based on the calculation according to the formulas and numbers reflected on the third sheet.

The declaration can be submitted in person, sent by mail or via the Internet.

If you have problems filling out, you can contact a specialized intermediary company that will not only draw up the document without errors, but also immediately send it in electronic form to the tax office.